Colin Read • November 26, 2023

A Giving Wage - November 26, 2023

This year I am fortunate to have two Thanksgivings. I visited my father, stepmom, brother, and sister-in-law for Canadian Thanksgiving, and had the opportunity to also see two close friends from high school that long weekend, one of whom is working to overcome a harsh medical diagnosis. Since then, Natalie and I celebrated American Thanksgiving with some close friends.

As I contemplate all for which we can be thankful, I harken back to high school half a century ago and what I imagined then the world might look like by now. Children of the Sixties were an idealistic lot, with service to humanity an important element that motivates many. I prefer to see the world as one large family. Of course, every family has its challenges, but we all recognize our shared DNA and aspirations.

Giving Tuesday on November 28 is but a few days away. Last week I was fortunate to participate in a panel discussion over a book about giving called “The Price of Humanity,” with author Amy Schiller. Throughout the discussion, I reflected that we have much for which we can be thankful as I found myself contemplating giving and the nature of human kindness.

Economics offers an interesting take on giving. The actions of government on our behalf should not be considered giving or generosity because government merely pools some of our collective resources to provide us with goods, services, and insurance that we cannot provide so easily for ourselves.

If we recognize few roads would be built if the public sector does not invest in them, only the most fortunate and elite would be educated in the absence of public schools, too many would fall off the societal cliff if it were not for our social welfare nets, and our nation maintains is sovereignty and public safety because of the police, courts and border defenses.

Some charities and foundations also provide for our collective good. They raise and spend money to provide better access to education, to research and develop new products and technologies, and further bolster our social welfare nets.

Collectively, these public and quasi-public agencies constitute around half of the economy in liberal democracies such as ours. That’s right. We are a mixed economy with private and public sectors of similar size.

The free market has consequences on income concentration that we accept as a nation because we recognize a couple of artifacts of a market economy. First, the incentive it provides to be industrious and innovative, and to determine the value of goods and services may not be replicable in alternative economic systems. Second, we are wary of the ability of government bureaucracies to respond as innovatively and efficiently as a market economy. For these reasons, liberal democracies tolerate some of the inequities of the market economies that drive half of our gross domestic product.

Let us assume that the other half of our economy which constitutes the public sector is able to operate efficiently to provide a specific balance of goods, services, and protections that democracies demand. The precise balance of such provisions, and of the size of the public sector relative to the free market sector we must presume is determined by the democratic process. Every nation will differ somewhat in these collective decisions. And each will determine a level of taxation to realize where we all intersect in our collective aspirations.

The question then remains whether we have an individual obligation to provide for each other beyond that we collectively provide through taxation and government spending. While nobody would label taxation as giving, all of us give back in other ways.

Our giving is motivated by many factors that can be ranked on a spectrum. On one end of a spectrum is indiscriminate giving for which I cannot ponder any example. On the other end is highly restricted giving for those causes that directly benefit the donor. Giving to a club for which I am a member, or to a church to fund its Sunday services might be giving to help myself.

Most all other giving lies between these two extremes. One may be afflicted with an illness and decide to donate part of their estate to fund research that can help those in the future enjoy a better fate. I may be grateful for the education I received and wish to create access to those who follow me, just as someone may have paved the way to public education for me in the past.

These forms of giving pay it forward by creating a better world I can enjoy, or pay it backward by thanking those in the past for their generosity by replenishing their fund of goodwill. We may do so because such giving makes us feel good. If such is the case, our giving is a form of consumption. We spend our income to generate our own happiness, even if we derive our happiness by generating happiness for others. If we assume that the maximization of our own satisfaction is a selfish act, then altruism is selfish, but in a good way that benefits others. For that reason, society considers altruism a virtue.

We may also give because we recognize it improves economic efficiency. Donations to public education are in this category because these investments will pay dividends in increased economic efficiency and productivity for generations to come.

These altruistic forms of giving and these investments in our collective future are all virtues we encourage as a society and economy. In fact, we subsidize them through charitable deductions in our tax code. However, these subsidies are perverse. The subsidy is in the form of a tax deduction in proportion to our tax bracket. A married couple with a combined income of around $650,000 are in the highest personal income tax rate of 37% in the United States, and upwards of 13% or more in some states. They receive a fifty cent tax rebate on each dollar donated.

On the other hand, most people with income less than about $250,000 are unlikely to donate any charitable deductions at all because their itemized deductions for state and local taxes and charitable giving are unlikely to exceed their standard deduction of almost $28,000 in the U.S. in 2023. Even if their state and local taxes and charitable deductions exceed this amount, the tax rate for a married couple who earns around $100,000 per year is less than 20%. This means that they receive a tax rebate for a dollar of giving of between zero and twenty cents, which average to a fifth of the subsidy given to wealthy donors.

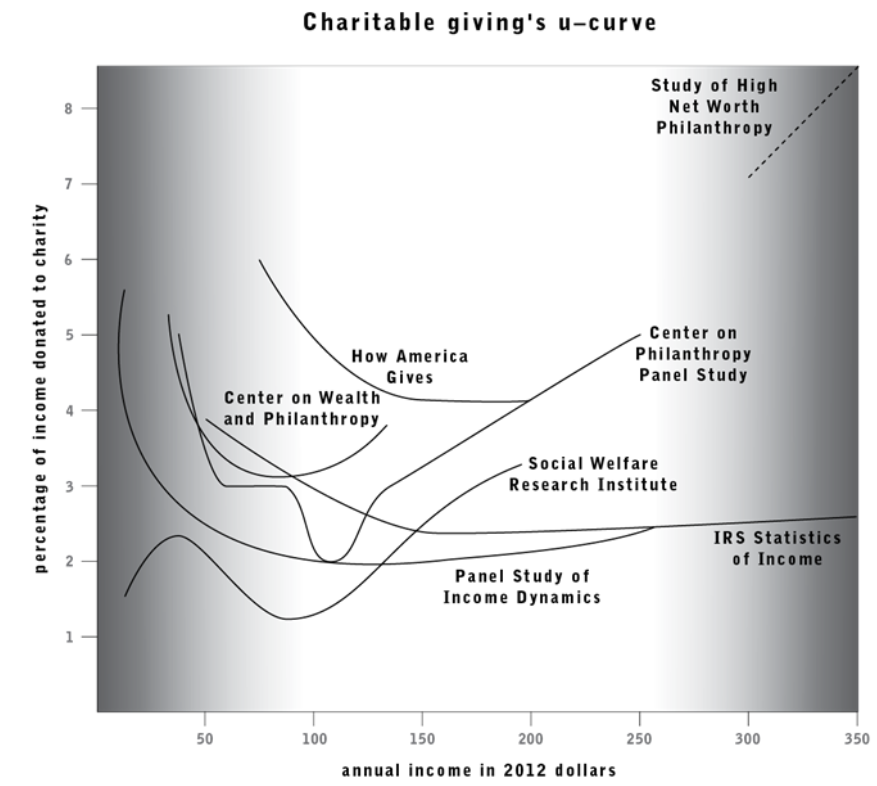

Economic intuition would suggest that the wealthy would then donate a greater share of their income than those of moderate or low income. But, they don’t. Those with income less than $100,000 are the most generous donors as a share of their earnings. In fact, they give more than twice their share of earnings as do the wealthiest. Economists measure how our consumption increases with income. Those items purchased in greater proportion as income rises are deemed luxury goods. Contrary to conventional wisdom, charity is not a luxury good.

The other surprising phenomenon is that the wealthy are more likely to donate a share of their income to art organizations and elite universities when compared to those in the bottom 10% of household income. In other words, poorer households tend to donate relatively more on the basic human needs side of the donation spectrum while the wealthy tend to donate more on the side of the spectrum that are more likely enjoyed by the wealthy themselves, such as elite colleges. One could argue that the poor donate to narrow gaps in society while the wealthy donate in ways that widen gaps.

Amy Schiller noted that some of these unexpected consequences could be easily changed through a slight modification in the tax code. Rather than have charitable incentives rise in proportion to one’s tax bracket by making them tax deductible, we could instead make charitable contributions eligible for a tax credit. If the average tax break across all income brackets is around 30%, a tax credit that provides thirty cents back on each dollar donated, regardless of tax bracket, may redress charitable giving inequities. It would be interesting and likely to see that such a change would result in more giving on the part of poor and middle income households who receive little or no subsidization for their giving. It may result in less giving from wealthy households, though, who already give less as a share of their income, despite the larger subsidization they receive.

Another tax tool worth consideration is reconsideration of the tax code on estates and inheritances. Lower income households typically have little, if any, to pass to their heirs. The wealthy can accumulate very large amounts to pass to their heirs tax free, and have many more sophisticated tools to ensure they can maintain their wealth across generations. Inheritance taxes less favorable for the wealthy may induce greater charitable contributions in their lifetimes.

Schiller argues effectively for a giving wage. We are familiar with the concept of a living wage that ensures every citizen can provide food and shelter for their families regardless of income, education, and the most marketable skills. What if the concept of an Annual Guaranteed Income, often spoken of as a response to the concern over income distribution as Artificial Intelligence replaces workers, was augmented to ensure an Annual Giving Income? If the poorest among us are already the most generous, we may find that providing some additional income to them as part of an Annual Giving Income will create even more charity.

Finally, what are we trying to accomplish with our charity? If government is designed to provide for those public goods that ensure a market economy can be both efficient and equitable, charitable giving can provide greater quality of life in ways that contribute to our social fabric and culture. Government can provide for what we collectively need, and our personal spending can provide for our individual wants. Giving can provide for our collective wants.

As Natalie and I walked our dog on a beautiful fall day in Plattsburgh today, we discussed in which ways we would like to give back. We have all worked hard as we moved through our lives and careers. But, none of us would have succeeded had it not been for the investments by others who came before us and the infrastructure our highly economically developed nations provided to us. We need only look to smart and hardworking people who suffer elsewhere because they did not benefit from the economy around them that we may take for granted here. Giving Tuesday a few days after Thanksgiving each year provides us with such an opportunity to reflect where we are and want to be on the various spectrums of giving.